With marine insurance being an important component of vessel operating costs, we have completed a review of the latest trends in P&I and H&M as part of the assessment for Drewry’s upcoming Ship Operating Costs report.

Protection & Indemnity

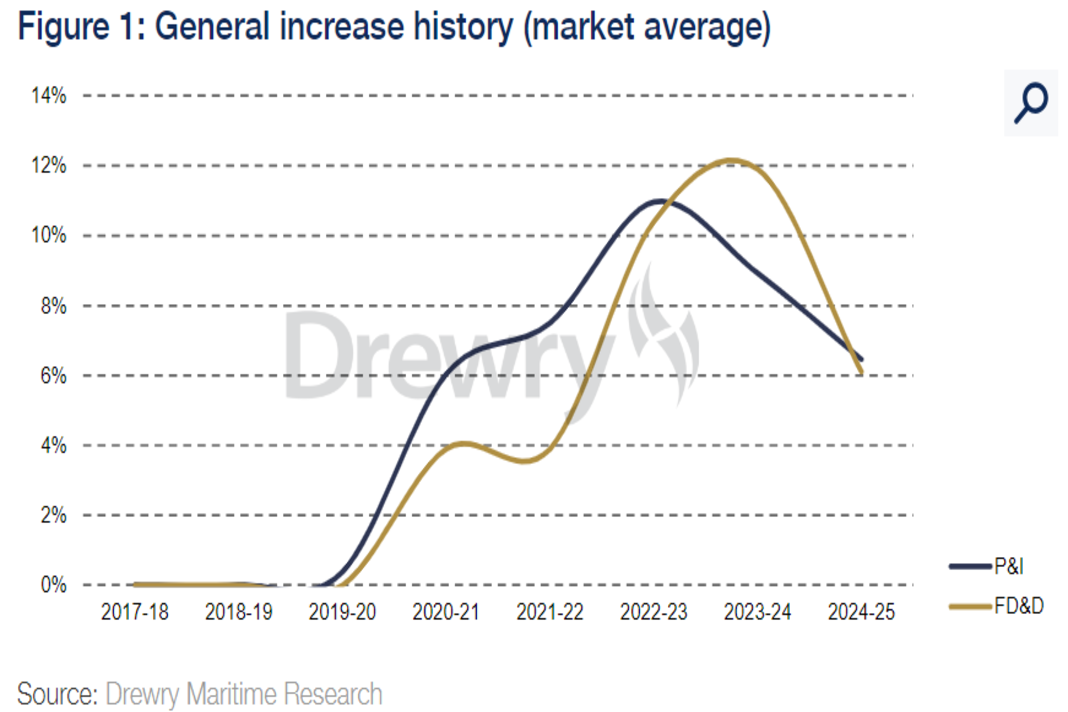

At the recent renewal on 20 February 2024, the International Group Clubs were seeking an average general increase of P&I 6.5% (FD&D 6.1%), with a range of 5% to 7.5%. Anecdotally, it seems likely that the clubs did not achieve this level of increase with positive indicative results for the 2023-24 year perhaps allowing a little flexibility concerning premium rating.

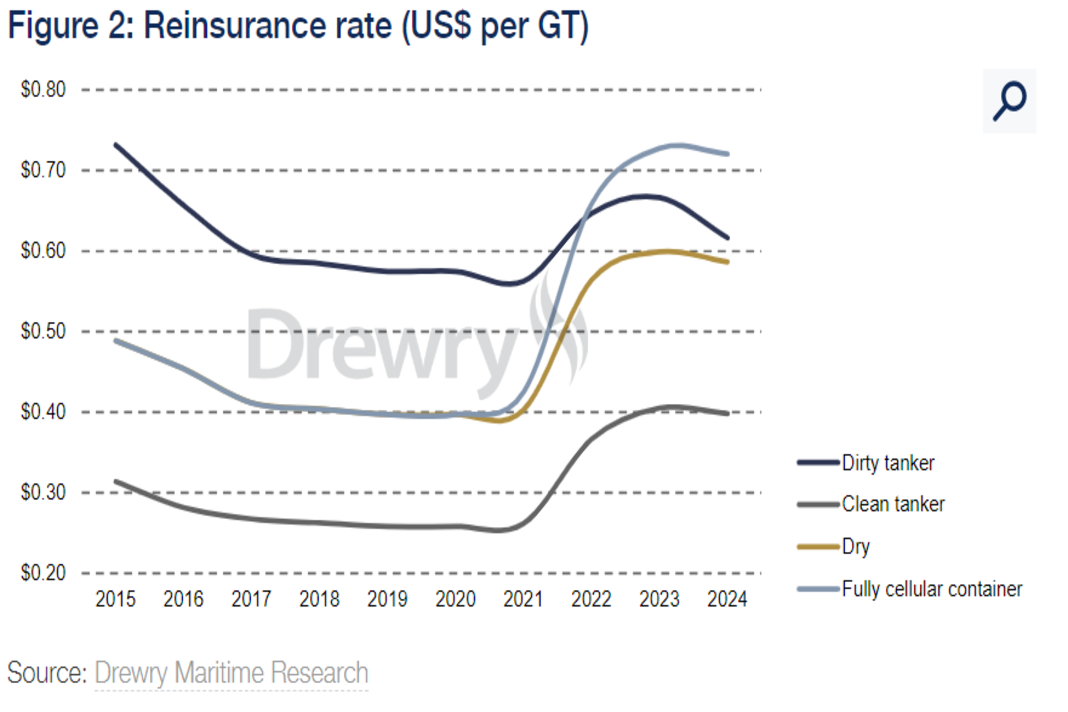

The reinsurance cost passed on to members has decreased slightly across each class of vessel by 1% to 2% except for passenger vessels (12.5%) and dirty tankers (7.5%) where more substantial reductions were seen. This element of overall member charge relates to both the ceded reinsurance program, more than $ 100 million – which essentially provides cover for very large or catastrophe losses -and to retained pool losses over $ 30 million, and so the recently improved pool loss experience in the past two years will somewhat dampen the impact of the commercial reinsurance market demands.

Hull & Machinery

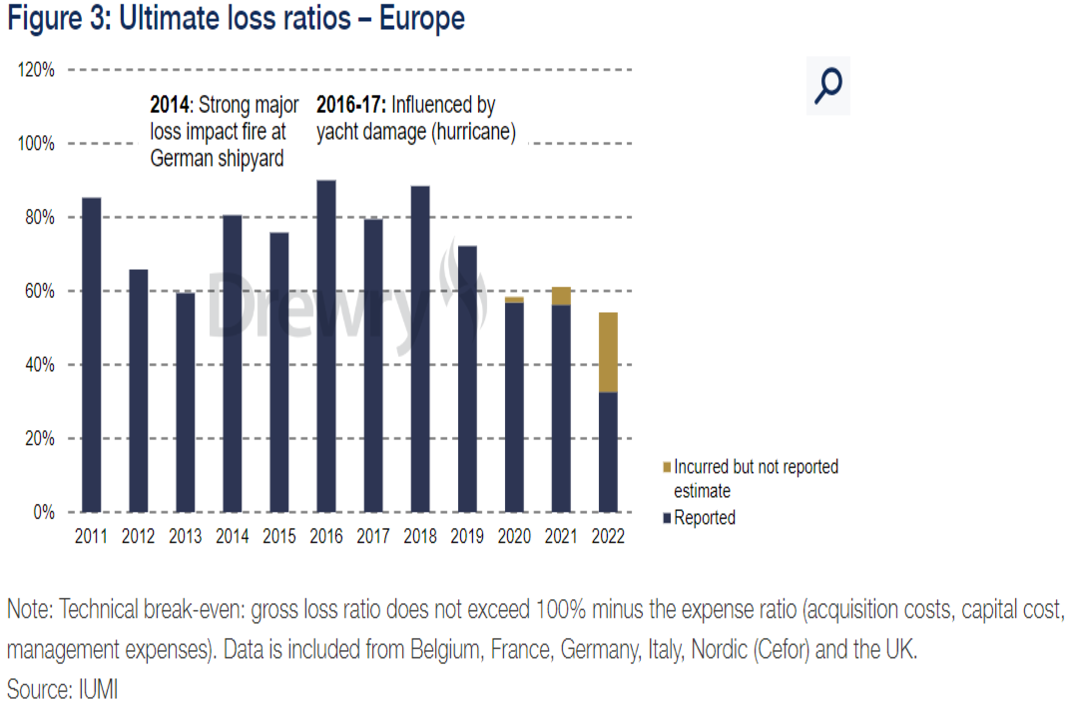

The last 6 or 7 years have seen loss ratios improving both due to premium increases and greater focus on underwriting integrity. During the COVID impacted period between 2020 and 2022, the trend was far from clear, but as global trade picked back up, it seems that the corrective action has had a positive effect and that claims frequency (particularly large claim frequency) has been an additional positive factor for both insurers and vessel operators.

Note that the above figures are loss ratios as opposed to combined ratios, but the trending is positive and we understand that the 2022 combined ratio would have been in the mid 90% – 100% range. Thus, underwriters may feel rates are currently adequate for so long as claims trends continue as is. Like it has been seen for P&I claims (particularly pooling claims), claims severity is perhaps more the primary driver than claims frequency. Whether this is down to increased deductibles or sheer good luck is hard to interpret.

New capacity entering the market in 2024, particularly via MGA’s, will start to pressurize rates, and may also lead to greater intensity of competition as they try to win market share. Similarly, London underwriters who lost market share during the period of rate correction may look to regain that share.

War Risks

By their very nature, premiums required for breach voyages are extremely volatile and may vary week to week as conflicts escalate and abate. During 2022 and 2023 underwriters appear to have made good returns on this class but with the onset of Houthi attacks in the Gulf of Aden and the Red Sea, premiums spiked substantially, and the added dynamic of targeted interests led to split rates depending on the ownership/management of the vessels and also upon where the vessel was sailing to/from.

This has resulted in many shipowners making the commercial decision to avoid the conflict areas and take the longer route around the Cape of Good Hope, which will take a significant premium out of the market. Not only has the primary war risk cost increased, but this uncertainty has also similarly impacted the cost of charterers and non-mutualized excess war risks.

Conclusion

Having regard to all of the above, it seems likely that there will be minimal impact across the board on owners operating costs as a result of insurance trends. The exception to this would be owners who repeatedly enter war zones and choose to pay short-term additional insurance costs to do so.

The unknown factor in this conclusion however revolves around how the insurance/reinsurance market responds to the allision between the “MV Dali” and the Francis Scott Key Bridge in Baltimore. If the vessel owners and managers are successful in their filing for limitation of liability, then substantial elements of the claim may fall on a different group of insurers and reinsurers, which could well influence premium rates going forward.

Did you subscribe to our daily newsletter?

It’s Free! Click here to Subscribe!

Source: Drewry

{kind=link}