The cost advantage of big containerships’ is reduced due to lower fuel prices.

The influence of change in the line’s cost structure of bunker prices resulted in the reduction in number of vessels per loop that would increase the effective slot cost.

Slow steaming and then super slow steaming were the effective modes of operation when the bunker prices rose dramatically in 2007/8. Later the global financial crisis reduced the market demand for fuel slow steaming and helped in soaking up the surplus vessels. When demand returned to more sustainable levels, lines continued with slow steaming because of the significant cost advantages not minding the cost of extra vessel.

The current bunker price is $100 per tonne, Drewry with its analysis has modelled the ship system costs (vessel, bunker, port and canal costs) for an illustrative Asia to North Europe loop, using 11, 10 or 9 ships to provide a weekly service, and with bunker prices at $100, $300 and $600 per tonne.

Speeds required for a weekly service depending on number of containerships deployed

Asia to North Europe slot cost vs number of vessels for various bunker prices

Highlights of the analysis:

- A reduction in the number of vessels per loop would increase the effective slot cost.

- There is a small change in slot cost if loop speed is increased, and the number of vessels reduced.

- There are clear cost savings by increasing service speed and reducing the number of vessels per loop.

And at present, as at the outset of slow steaming, there is an excess supply of tonnage, which would only be exacerbated if more ships were released as a result of speeds being increased.

On the other hand, with bunkers being relatively cheap, we may see other steps being taken by lines:

- Extra calls may be added to loops, as the incremental cost of faster steaming will be lower.

- Schedule reliability should improve (as is already happening) – lines should be more willing to pay the cost of speeding up to achieve an on time arrival.

- A carrier and/or alliance may see this as an opportunity to gain a marketing advantage by offering a fast transit service on key routes, using the additional speed capability of their vessels.

While sudden change is unlikely, lines should be aware that the ongoing surplus of tonnage will get worse if there is a trend to remove ships from loops.

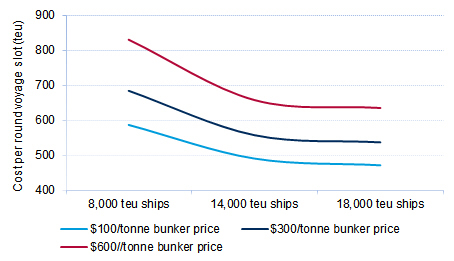

Figure 3

Asia to North Europe slot cost vs vessel size for various bunker prices

- This reports that as the vessel size increases the cost per round voyage decreases.

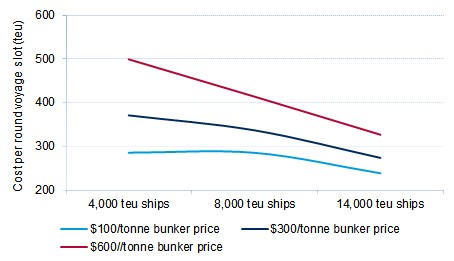

Figure 4

Asia to US West Coast slot cost vs vessel size for various bunker prices

- Using a current market charter rate for a Panamax 4,000 teu vessel of $12,500 per day, shows that the slot cost saving of 17% at a bunker price of $600/tonne diminishes to zero at a bunker price of $100/tonne. This is still relatively low, is higher than the rock bottom rates being earned in 2013/2014.

Source: Drewry Shipping Consultants Ltd

{kind=link}