As water levels rise in the Panama Canal, so too do hopes that ocean freight container services can return to business-as-usual following more than a year of restrictions due to drought.

However, these hopes should be accompanied by a dose of realism. While the situation is improving, there is still a long way to go before transits return to the level seen before the first restrictions were imposed back in February 2023.

On 16 May, the Panama Canal authorities will increase the total number of ships that can transit this vital supply chain chokepoint each day from 24 up to 31.

These additional seven transits will provide limited benefit for container services because they are for ships with a beam not exceeding 107 feet and no bigger than the traditional Panamax ships.

There will be more meaningful change for container services on 1 June when one additional transit will be allowed for Neopanamax ships, rising from seven to eight each day. This will take the overall number of daily transits from 31 to 32.

Carriers make a return to Panama Canal

While numerical restrictions do matter, what is perhaps of more importance for container services are the draft restrictions (primarily for Neopanamax locks), which restrict the amount of cargo that can be carried on each ship.

Fortunately, there is good news on this account as well because on 15 June the draft limitations for ships transiting the Neopanamax locks will increase from 44 feet to 45 feet. Carriers and shippers will be looking forward to the day when it reaches 50 feet, which is the normal, undisrupted draft limit.

The improving picture has tempted some ocean freight container carriers to return to the Panama Canal.

For example, Yang Ming lines has been avoiding the Panama Canal for its Asia to US East Coast and Gulf Coast services since Q4 2023. However, six months later it has decided to return.

Similarly, Maersk Line has been operating a rail-land bridge on one service as an alternative to transiting the canal but returned to an ‘all-water’ transport offering on 10 May 2024.

Schedule reliability remains disappointingly low

This return towards a semblance of normality cannot come soon enough for shippers, freight forwarders and carriers who have all paid the price for troubled waters in Panama – particularly in terms of schedule reliability.

Using the Far East to US Gulf Coast trade as an example, schedule reliability hovered around 60% pre-pandemic. It then plummeted to 20% during the pandemic before recovering to 40% as the impact of Covid-19 began to alleviate.

It has remained around that level ever since in no small part due to the situation in the Panama Canal, with three out of five ships arriving late at the destination by more than one day. The number of days these ships were late has also increased from three days pre-pandemic to six days currently.

Impact of Panama disruption on rates

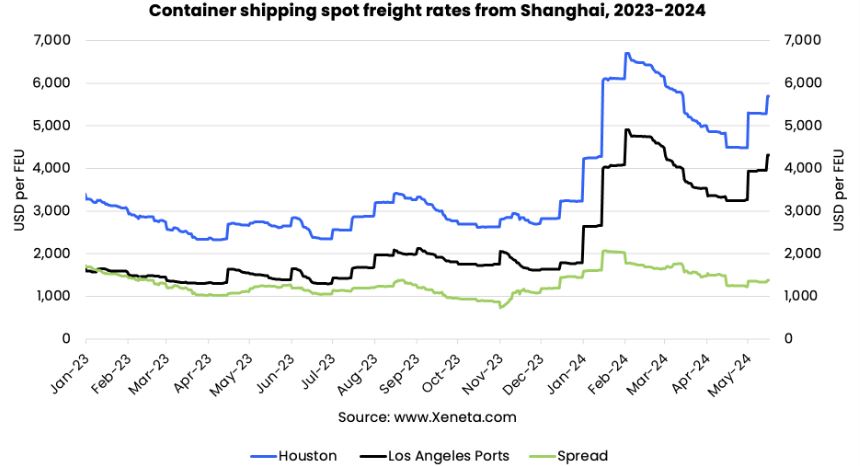

The impact of disruption in the Panama Canal can be seen in the spread of spot rates on the trade from Shanghai to Houston compared to Shanghai to Los Angeles Ports.

Xeneta data shows that in January 2024, when the Panama Canal drought was causing the most severe operational disruption, the spread in the spot rates paid by shippers on these two trades exceeded USD 2 000 per FEU (40ft equivalent shipping container).

This was the highest the spread had been since November 2022 and demonstrates the measurable impact disruption at a vital artery for world trade can have on the cost of ocean freight container shipping.

The January peak of 2024 possibly came as a more severe shock to the market given it was just two-and-a-half months after the spread dropped to a multi-year low at the end of October 2023. This reversal of trend coincided, almost to the exact date, with the Panama Canal authority’s announcement of a ‘roadmap’ to address the Gatun Lake water shortage.

A return to ‘normality’

For some people this roadmap felt like a draconian measure, but to the more informed logistics professional it was an inevitable step that was perhaps overdue.

This roadmap outlined additional restrictions over the next four months which saw transits fall from 32 (which had been in place since 30 July 2023) down to just 18 in February 2024. This increased clarity allowed businesses to better plan ahead, rather than taking the naïve approach of hoping for the best, while fearing worse.

Fast forward to today and the easing of restrictions and return of carriers to the Panama Canal has impacted rates. On 13 May, the spread in average spot rates between the Shanghai to Houston trade compared to Shanghai to Los Angeles Ports had reduced to USD 1 319 per FEU. However, this is still higher than the USD 873 per FEU seen at the end of October last year.

Hopes of a return to a ‘normal’ market very much depend on what is considered normal – and this is certainly a moving target which develops over time as trade flows evolve.

Back before the Covid-19 pandemic when the Asia to US Gulf Coast trade lanes were relatively less mature, the average spread in the trades from Shanghai to Houston and Shanghai to Los Angeles stood at USD 1 475 per FEU. In 2022, the spread peaked at USD 3 860 per FEU.

However, since exceeding USD 2 000 in January 2024, the spread has reduced with the average year-to-date figure standing at USD 1 606 per FEU.

The Asia to US Gulf Coast trades are now more mature and the spread in the trades from Shanghai to Houston and Los Angeles should fall back below the pre-pandemic level seen in 2018-2019. However, volatility is still to be expected (as is the case on many of the world’s main trades due to geo-political and climate related black swan events).

Panama Canal drought in numbers – ships and locks

On 1 February 2023 the first restrictions were announced, coming into force one month later, with maximum draft for ships transiting the Neopanamax lock reduced to 49.5 feet (normal draft 50 feet). This eventually reduced to 44 feet.

The lowest number of transits occurred on 8 January when just 18 ships passed through the canal.

When measuring daily averages across the month (both directions), 2023 saw 35.97 ships transit the canal each day, out of which 9.26 were of Neopanamax size. 2024 only saw 21.94 ships transit the canal each day (-39.7%), out of which 5.97 were Neopanamax size.

Looking at container ships only and measuring daily averages across the month, 2023 saw 7.39 ships transit the canal, of which 4.19 were Neopanamax size. 2024 saw only 6.58 container ships (-11.0%) transit the canal, out of which 3.77 were Neopanamax size.

The smaller reduction for container ships (-11.0%) compared to all vessels (-39%) is an indication of the fact that container ships receive preferential treatment for transiting the Panama Canal.

Hopes may rise, but reality may be different

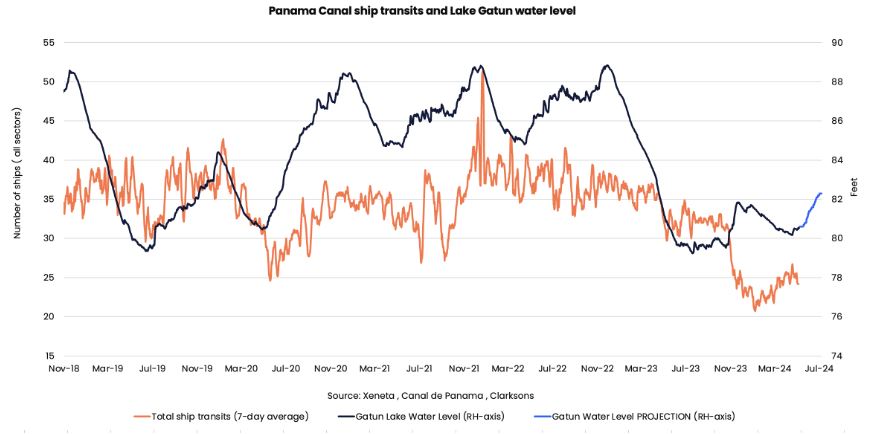

The graph below combining the Gatun Lake water level with daily ship transits clearly demonstrates the severe impact drought has had – and continues to have – on ocean freight services.

Xeneta has long-held the position that the impact of drought in the Panama Canal will be felt for years rather than months. Back in 2023 when drought first hit the headlines, the Xeneta position took some observers by surprise who expected the situation to resolve itself once the rainy season arrived.

The situation is clearly improving and compared to a fortnight ago the Gatun Lake water level is half a foot higher. But only allowing 31 ships to transit is still impairing businesses with supply chains which transit of the Panama Canal – especially at a time when the Suez Canal is being avoided by the majority of container ships.

Hopes will continue to rise that the Panama Canal can return to normal, but it will be a slow process and rely on rainfall, which is a factor people may try to predict but no one can control.

Did you Subscribe to our daily newsletter?

It’s Free! Click here to Subscribe!

Source: Xeneta

{kind=link}